- Company

-

Investor Centre

- Our Performance ASX Announcements Investor Presentations Key Financials News Results Centre Share Price

- Shareholder Information Annual General Meetings Dividends/Special Distributions Financial Calendar Green Finance Framework Recall Demerger Shareholder Services Shareholder Communication Options TCFD Disclosure

- Corporate Governance

-

Sustainability

- Our Sustainability Strategy Our 2025 Sustainability Targets Our 2020 Sustainability Goals Our 2020 Goal Achievements Our net-zero roadmap

- Reporting & Governance ESG Navigator Global Reporting Initiative Index UN Global Compact Sustainability Governance Sustainability Review Sustainability Case Studies

- Contact us

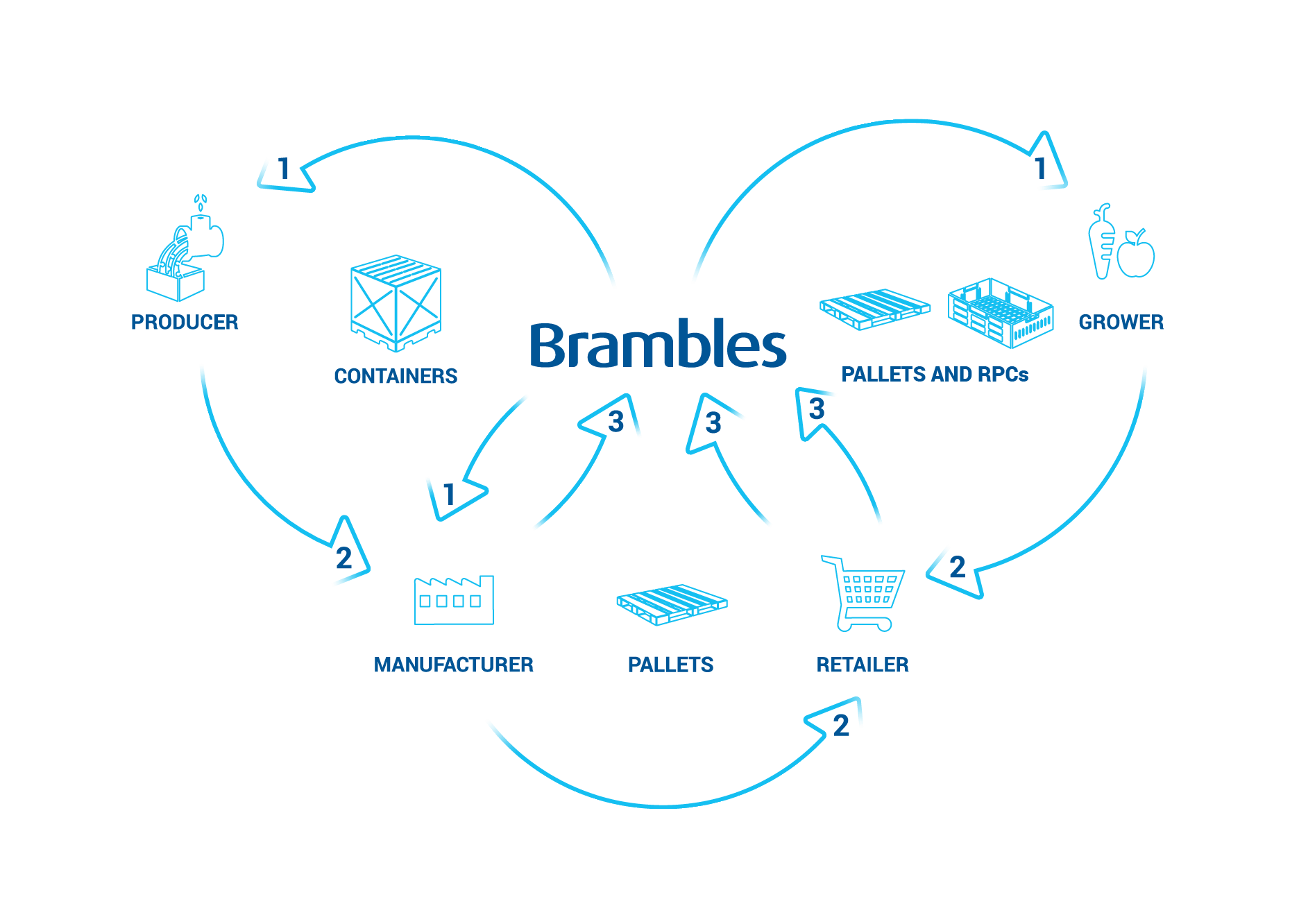

Inherently Sustainable Operating Model

Brambles’ ‘share and reuse’ model follows the principles of the circular and sharing economies, creating more efficient supply chains by reducing operating costs and demand on natural resources. By promoting the ‘share and reuse’ of assets among multiple parties in the supply chain, Brambles offers customers a more efficient and sustainable alternative to the use of disposable single-use alternatives or managing their own proprietary platforms.

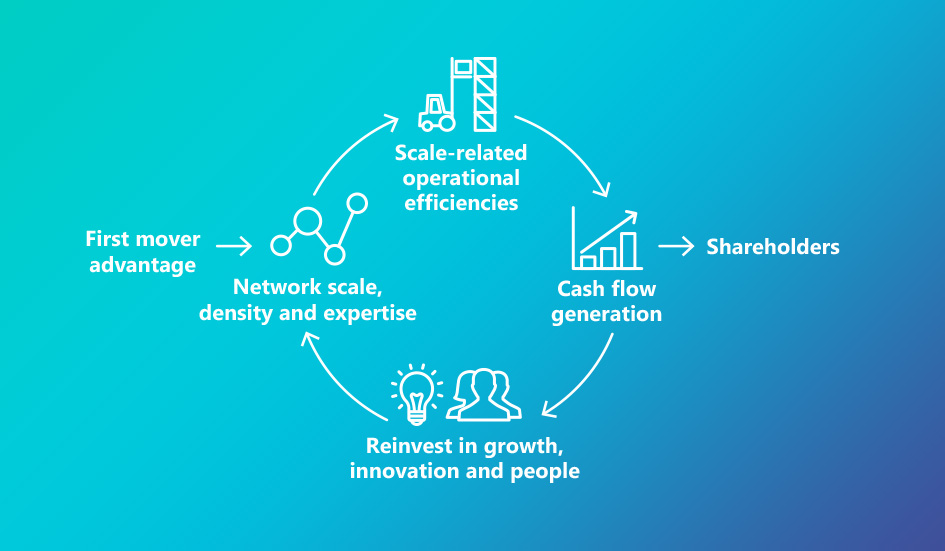

Network Advantage and Supply Chain Expertise

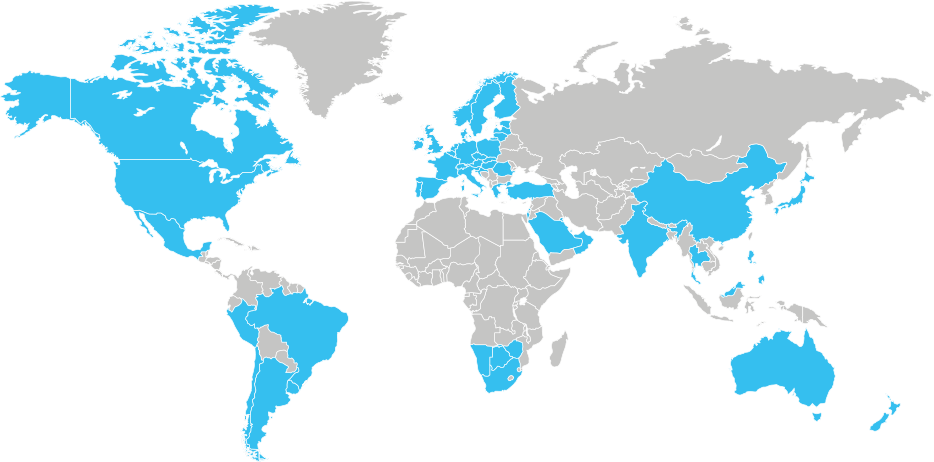

Brambles’ sustainable operating model is underpinned by its superior network advantage and industry-leading supply chain expertise, developed over 70 years of managing customers’ supply chains around the world. With operations in approximately 60 countries, Brambles’ network advantage comprises the scale and density of its service centre network and the strength of its customer relationships in every major market in which it operates. This means Brambles can be faster and more responsive to customers’ needs and in times of uncertainty and increased volatility, more resilient and more reliable.

Transformation to Strengthen Competitive Advantage

Through the Shaping Our Future transformation programme, Brambles is investing to build on its existing competitive advantage by enhancing operational efficiency and increasing the value created across its customers’ supply chains. Investments to build the 'Brambles of the Future' include developing new business capabilities and identifying new sources of growth that will allow the business to stay at the forefront of innovation.